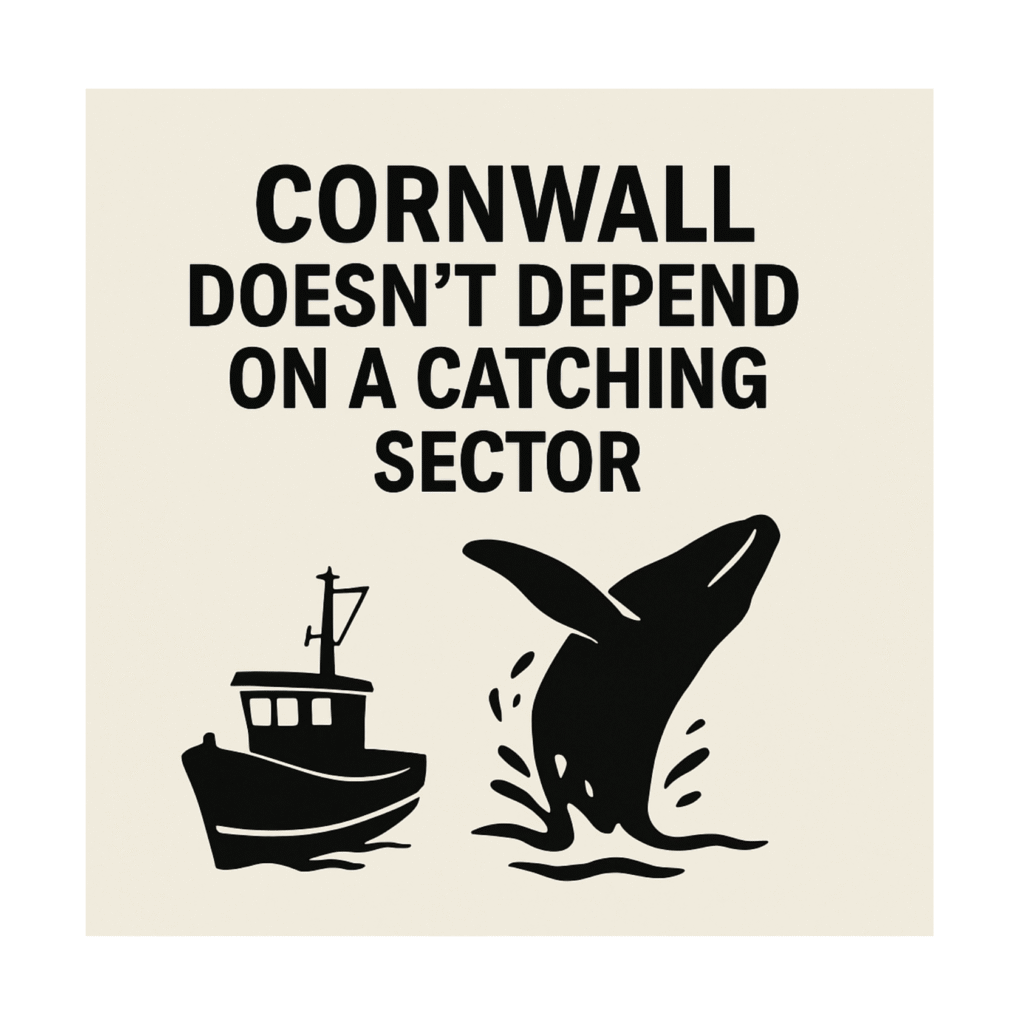

Cornwall’s Seafood Economy: Beyond the Catch

Cornwall fishing’s lobbying report “Value of Seafood to Cornwall” paints a picture of a seafood sector utterly dependent on the catching fleet1. It notes ~7,800 local seafood jobs (2.9% of Cornwall’s workforce vs 0.7% nationally) and claims every onshore seafood job is ultimately tied to fishing. By using the statement “For every job in the CIoS catching sector, there are 15 more jobs across Cornwall and Isles of Scilly in other seafood sub-sectors.” It infers a direct link between the catching sector and the other jobs, as if each individual catching sector job supports the rest. Economic data tell a different story. Nationally, and in Cornwall, most fish eaten come from abroad, and visitors, not fishermen, form the backbone of the coastal economy. Policymakers should heed the full picture: Cornwall’s seafood industry can thrive even as catches are constrained, and overfishing today threatens far greater revenues from tourism and recreation tomorrow.

1. cfpo.org.uk

Imports Dominate UK Seafood Consumption

UK Government data makes clear that the UK relies overwhelmingly on imported seafood. Since the 1980s the UK has been a net seafood importer2. In 2021 the UK imported 791,000 tonnes of fish (worth £3.3 billion) but exported only 363,000 tonnes (£1.6 billion), a trade deficit of £1.7 billion. In other words, much of what Cornish shops and restaurants sell would have been sold anyway even if local fish stocks were low. Indeed, an estimated 60–80% of UK landings are sent overseas, while the five “Big Five” species (cod, haddock, salmon, tuna, prawns) that dominate UK diets are almost entirely imported.

2. researchbriefings.files.parliament.uk

Even industry voices concede this shift. Seafish (the UK seafood levy funded lobbying body) itself noted in 2006 that “only a relatively small proportion of the fish now consumed in the UK is caught by the UK fleet” and that “the health of the UK catching sector is no longer of such central importance to the UK seafood industry”. In practice, this means Cornish processors and fishmongers routinely rely on non-local supplies. The CFPO report itself admits that “processors, wholesalers, retail and foodservice outlets handle local seafood and also import prepared seafood from the rest of the UK and from overseas”. In short, the Cornish seafood value chain is globally connected, it will simply draw more on imports if local catches fall.

Cornwall’s Economy: Tourism vs. Catching

In Cornwall, tourism and hospitality dwarf the fishing sector in scale. The CFPO report’s own numbers show the entire Cornwall & IoS seafood industry (catching, processing and supply chain) contributes about £174 million GVA in total (≈1.5% of local GVA). By contrast, Cornwall’s visitor economy is worth ~£2 billion annually (about 15% of the regional economy)3. In jobs terms, Cornwall’s food-tourism sector employs roughly 35,700 people, nearly five times the ~7,800 seafood jobs noted by CFPO. These figures underscore that Cornwall’s prosperity depends far more on attracting tourists (many of whom eat seafood) than on the volume of fish landed.

3. cornwall-opportunities.co.uk

Cornish restaurants, cafés and hotels will continue serving seafood, and employing people, even if more of that fish comes from Scotland, Norway or fish farms. The CFPO report concedes that processors handle imported species when “not available in quantity in CIoS”. In practice, this means local seafood outlets already substitute imported cod, prawns, tuna, etc., to meet demand. The catching fleet’s identity and tradition aside, Cornwall’s onshore jobs and businesses don’t vanish if Cornish boats dock, they simply source fish elsewhere. Put bluntly, a Cornish fish and chip shop will keep selling cod regardless of whether it was caught in Cornwall or imported, supporting staff and the local supply chain either way.

The Rise of Recreational & Nature-based Income

Crucially, Cornwall’s coastal economy stands to gain far more from recreational fishing and wildlife tourism than from pushing for bigger catches. Recreational sea angling alone is a multi‐billion-pound UK sector. The Angling Trust reports that UK sea anglers spend roughly £1.5 billion per year, directly supporting about 15,000 jobs (in tackle shops, guides, charter boats, etc.) and injecting up to £847 million into local coastal businesses (hotels, restaurants, B&Bs)4. A healthy fish stock multiplies this effect: charter-boat customers buy bait, fuel, lodging and meals. By contrast, fishermen’s direct first-sale income (only ~£44 m in Cornwall last year) is tiny next to the tourist spend.

Marine wildlife tourism is another growing source of income. Whale and dolphin watching in Cornwall attracts thousands of visitors (for example, the popular “Sea Safaris” out of Padstow) who pay for boat trips and patronise local services. Like angling, these activities pay the bills only if fish stocks and ecosystems are robust. Indeed, wildlife organisations note whales “are worth considerably more alive than dead,” since their presence generates longer-term tourism revenue. Encouraging catch recovery (through quotas, protected areas, low-impact gear, etc.) would directly benefit these sectors. In short, valuing fish more in the water than on the deck would unlock far more jobs and spending for Cornish communities.

Policy Implications: Diversify, Don’t Double-Down on Catching

Policymakers should treat Cornwall’s marine economy holistically. The CFPO report’s message, “if you don’t have fishing, you don’t have communities”, rings hollow next to the broader data. In reality, Cornwall’s communities and economy rely on a mix of imports, processing, aquaculture and tourism as much as on local catch. For example, Cornwall’s mussel farms, oyster fisheries and even emerging seaweed aquaculture add jobs without pressuring wild stocks. Likewise, value-added processing (smoked fish, ready-meals) can use imported or farmed fish while still employing Cornish workers.

Rather than propping up the catching fleet, the government should invest in marine resources as public goods. Measures that rebuild fish populations, such as well-enforced quotas, no-take zones and bycatch reduction, will boost recreational angling and eco-tourism, directly benefiting Cornwall’s economy. Schemes that diversify seafood supply (e.g. developing domestic aquaculture or supporting port infrastructure for imports) will also fortify jobs. In essence, Cornwall’s seafood industry can continue to thrive without expanding local catch, and indeed thrives more when stocks are plentiful.

In conclusion, the CFPO report provides important local data but its implied prescription (more catch = more prosperity) is misleading. A thriving Cornwall needs healthy seas and diverse marine activities. By focusing on sustainability and the larger tourism/leisure economy (which, as Seafish noted, now eclipse the catching sector’s role), policymakers can secure long-term jobs and income for Cornwall, far beyond what chasing extra landings would ever yield.